This result applies only to FIAs that have point-to-point “capped” payoffs.

In this analysis, we show that buying one point-to-point hedge (call spread) at the weighted average strike (cap) is far more advantageous than buying multiple hedges at different strikes. Using historical market data for S&P 500 index, we prove that this result holds true in every scenario of liability weights.

Let’s understand by example.

Let us assume that the risk manager is looking to hedge three FIA liabilities, each of $100,000 notional (principal) at caps of 5%, 7% and 9%. The weighted average strike of the single composite hedge will be 7% for $300,000.

If the cost of buying three individual hedges is the same as the cost of buying one composite hedge, the risk manager may presume that it is advantageous to buy three different hedges, since the three hedges will ‘mimic’ the liabilities exactly and will have zero basis risk and full hedge effectiveness. In practice, most risk managers do some averaging of the strike, but still buy many point-to-point cap hedges, rather than just one single hedge. We propose that they will benefit from buying just one hedge per index (and tenor) on their hedging day.

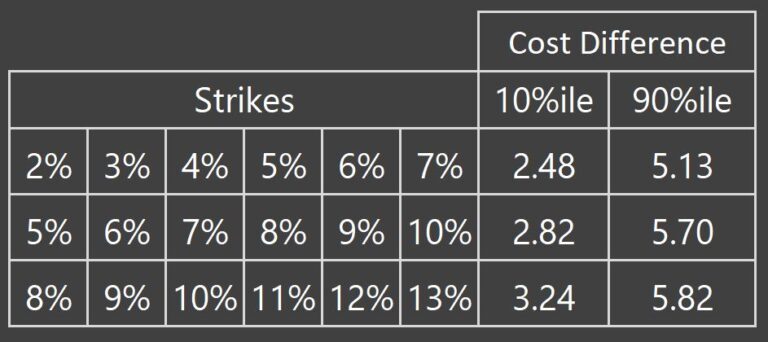

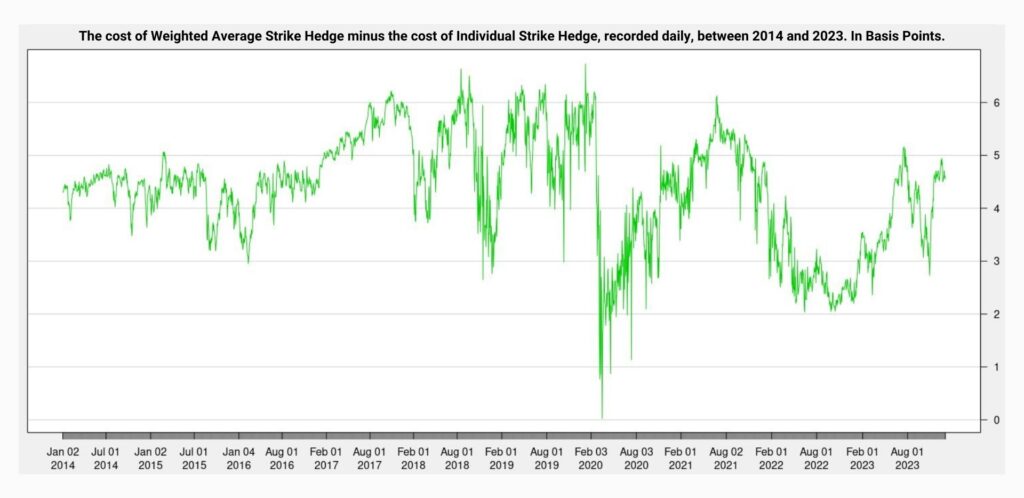

This single PTP hedge will be struck at the weighted average strike and will hedge all the policy allocations linked to a particular index and renewing on a particular date. We have determined that this single hedge will be 3 to 6 bps costlier than the sum of costs of the individual hedges, but will have a far higher realized payoff than the individual hedges. This single hedge will have zero additional basis risk, and will not decrease the hedge effectiveness either.

The reason behind this advantage is that this ‘averaging’ of strikes (caps) brings down the required return of the index. So, considering our sample case mentioned above, if the index returns 7%, buying one composite hedge will have a payoff of $21,000 (7% payoff), while the three individual hedges (struck at 5%, 7% and 9%) will have a payoff of $19,000 ($5000 + $7000 + $7000 ; 6.33% payoff). So, our single composite hedge returns a full 66 bps higher return than the individual hedges. Moreover, this 66 bps advantage is a ‘profit’ for the insurer since the interest credited to the policyholder’s account is still $19,000.

Mathematically, if the index return is higher than the minimum strike and lower than the maximum strike, the average strike hedge performs better than the individual hedges. As it is the case today, insurers have policies issuing and renewing at caps ranging from 4% to 12%, and this strategy is particularly effective.

To help you understand and test this result better, we are providing an Excel file.