Cost Synergies with bundling RILA Floor and RILA Buffer

Summary

In this article, we suggest how insurers can save on hedging costs for RILA by taking advantage of the naturally synergistic relationship between RILA Buffer and RILA Floor product design.

Hedging a RILA Buffer annuity requires selling an out-of-the-money put, while hedging a RILA Floor annuity requires buying out-of-the-money put. If the insurer can offset these two puts (long + short) internally, then trading them might not be required, potentially saving the insurer over a dozen basis points which can be put to work elsewhere. There are other strategic advantages to this hedge design, which are discussed below.

The key insight here is that if certain conditions are met (easily), then the short OTM put of Buffer and long OTM put of Floor cancel each other out. The insurer still has to account for them in the hedge budgets, but the actual transactions (buying and selling) are avoided. The conditions are: 1. Floor and Buffer have the same index and tenor (typically 1 or 2 years) 2. Floor and Buffer have the same strike (say 85% of at-the-money index level) 3. Floor and Buffer have similar allocations.

Conditions # 1 and #2 are easily and automatically met given the current design of RILA products at most insurers. Condition # 3 can be met by offering Floor and Buffer allocations together via a packaged deal, and/or by offering an additional discount for assigning equal capital into each of the two allocations (Floor and Buffer). Transactions can still be minimized by making the allocations approximately similar, if not completely equal.

To better understand the strategy, follow the images in order, i.e., Figure 1, followed by Figure 2 and finally, Figure 3.

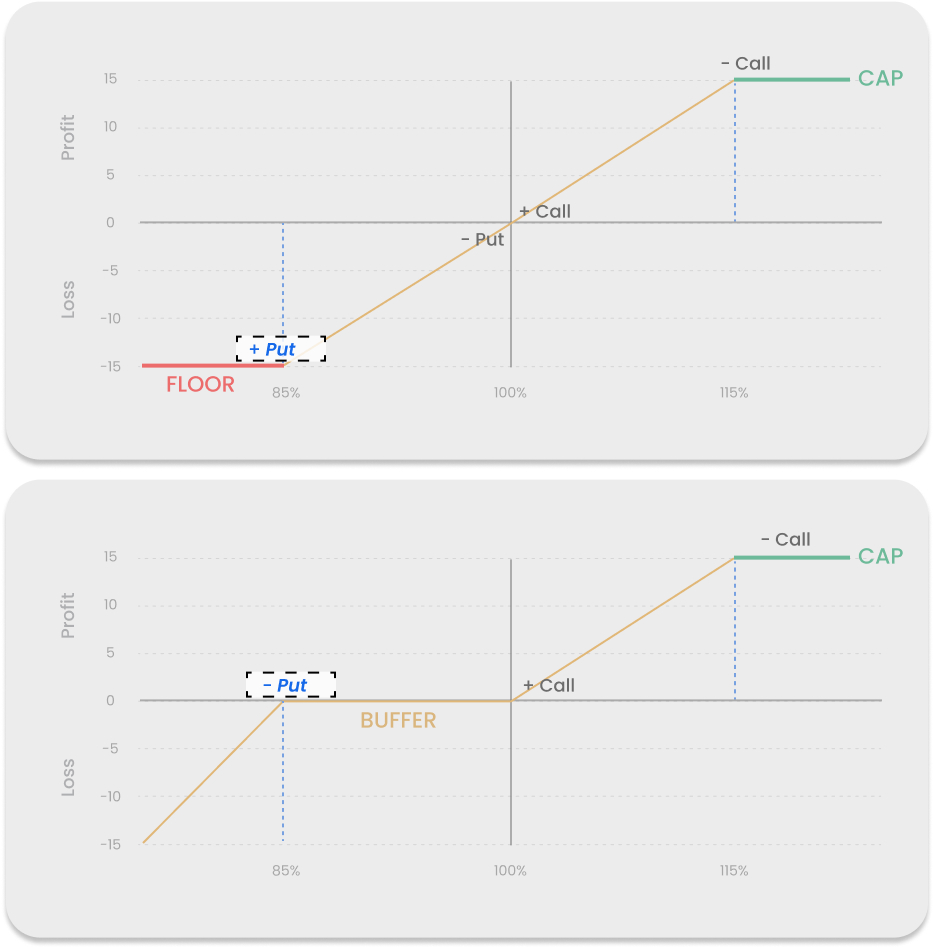

Figure 1 : RILA Floor and Buffer designs are shown via Option Payoff Diagrams. Cap is set at 15%, and Floor and Buffer both are set at 85%. With RILA Floor, the loss is Floored at 15%, and the investor cannot lose more than 15%. With RILA Buffer, the first 15% losses are Buffered, and the investor suffers losses only if the index loses more than 15%.

Figure 2: RILA hedge design is shown in detail. RILA Floor requires a Call Spread (+Call and -Call) and a Put Spread (+Put and -Put). RILA Buffer also requires a Call Spread (+Call and -Call) but only a Short Put (-Put).

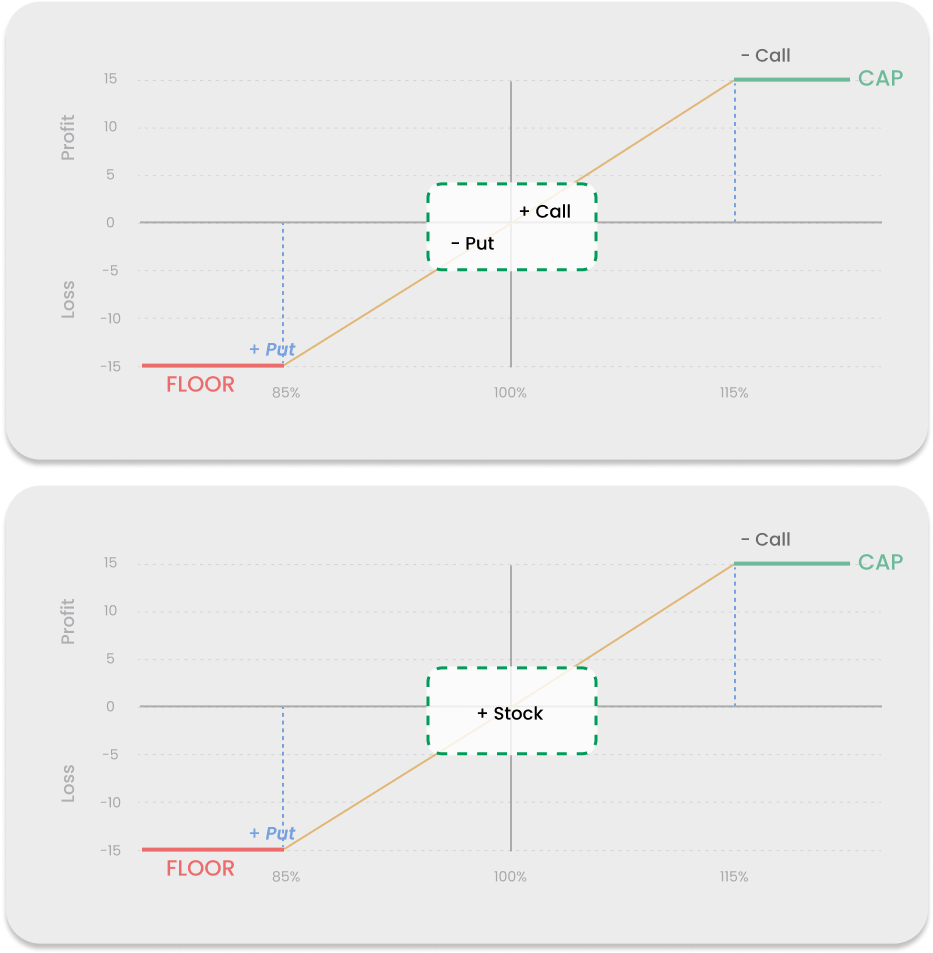

Figure 3: Long Put of the RILA Floor can be combined with the Short Put of the RILA Buffer. Both puts are typically exact opposites, being of the same index, strike and tenor. By avoiding the trading of these illiquid puts, insurer can save upwards of 10 bps in hedging cost.

When long OTM put and short OTM put cancel each other out, several advantages appear.

Insurers save upwards of 10 bps in transaction costs

By avoiding trading of the long put and the short put, insurers can expect to save upwards of 10 bps in transaction costs in even the most liquid SPX Index options. For 1 year tenor SPX European Vanilla options, near the cap of 10%, a 10 bps extra budget buys approximately 28 bps of extra cap as of this writing (Mar 29th, 2024). Meaning a 10 basis points of additional budget (obtained from foregoing trading of OTM puts) allows the insurer to increase the cap by 28 basis points. Likewise, for MSCI EAFE Index, an additional 10 bps of option budget buys an extra cap of 45 bps (as of Mar 29, 2024). These estimates may vary slightly in the future due to variation in skew levels.

When long OTM put and short OTM put cancel each other out, illiquidity of the OTM put is no longer a problem, which creates the following advantages.

Insurers are free to chose ETFs and custom indices for their RILA product suite

Many ETFs are amenable to RILA strategies, yet insurers are hesitant to consider them given the illiquidity and the hassle of trading puts. Derivative desks are also hesitant to commit to selling puts on illiquid ETFs and smart beta indices. With this new hedge design, insurers would be free to chose the index that best compliments their annuity product portfolio irrespective of the liquidity of the index (or ETF) in the option market.

Insurers are free to chose the strike of OTM put

Insurers typically choose the Floor or Buffer level at 90% or 85%. This floor/buffer level becomes the strike of the OTM Put.

Liquidity, particularly open interest in puts in the CBOE, is typically anchored to psychologically significant index levels (such as S&P 500 Index levels of 4000 or 5000). The insurer can take advantage of such psychologically significant levels in their marketing efforts. Rather than marketing some percentage (such as 80% of 5254 = 4203), insurers may benefit from marketing a significant index level (such as 4000 for S&P 500 Index, or 2000 for MSCI EAFE Index). If an insurer adopts this strategy, then the OTM Put strike becomes a theoretical reference point where the put needs to be priced but not traded. Potential RILA buyers, especially young buyers who also have brokerage accounts and stock / ETF investments, may find these numeric index levels (such as 4000 or 5000) in Floor or Buffer products more agreeable with their own mental accounting models.

Addtional savings may be obtained by combining Long ATM Call and Short ATM Put into a unit of stock or future, as is shown in Figure 4.

Figure 4: By combining the Long ATM Call and Short ATM Put into a Stock or Future, insurer can save even more.

The basics

Registered Index-Linked Annuity (RILA) are a special type of Index-Linked Annuity that offers higher-return and higher-risk relative to a fixed indexed annuity (FIA). The key difference between FIAs and RILAs is that during the deferral mode, while both FIAs and RILAs credit interest into policyholder’s annuity that is linked to the stock market (equity index), FIAs can never have negative interest no matter how much the index goes down, but RILAs can have (limited) negative interest credits. For this reason, RILAs are “registered” securities, since SEC classifies them as securities because they expose the policyholder to potential market losses.