In this analysis, we attempt to create an inflation-protected annuity by adding an increasing annuity to a level annuity. Increasing annuity’s annual benefit increases as {k, 2k, 3k, …} and so on. Final annual benefit amounts are {b+k, b+2k, b+3k,…} and so on.

To determine k, we simply ask the question – what value of k will be required to keep up with a given inflation rate and a discount rate.

This product is quite simple to build and simple to explain to an annuitant. We test this design using the 2012-IAM-Male table (unadjusted by G2 projection).

We find that:

The upfront premium (reserve) of such an inflation-protected annuity is much greater than a simple whole-life immediate annuity, and the benefit is backloaded, making this product somewhat less appealing to a policyholder who prefers bequest.

Given low annuitization rates (annuity puzzle), it might still be worthwhile for annuity providers to offer such a design as it will add to their product assortment and push out the demand curve.

Assumptions

Flat and unchanging inflation rate and discount rates. Monetary policy is slightly accommodative where the discount rate is (1% – 2%) less than the inflation rate.

Inflation protection ends after 25 years (20 years) for annuity starting at age 60 (70).

Last Survivor: 2012 Individual Annuity Reserve (Male) table (unadjusted for G2) is used for both annuitants. The last survivor receives 100% of the benefit amount. The same table (2012IAM-Male) is used for all other annuity payout calculations. Annuity is paid in arrears (not advance).

Motivation

The one thing that is truly disastrous for a retiree’s portfolio is persistent inflation. And today’s inflation is definitely not transient. As of this writing (Oct 9th, 2022), fed funds are at 3.25%, US Treasury 2-year yield is at 4.30%, inflation is at 8.3%, and unemployment rate is at 3.5%. The last time we saw such a surge in inflation in the US, it persisted for 2 decades (1968-1990 approx.), and it took almost 4 business cycles for the inflation to be wrung out of the US economic system altogether. The young workforce may revel in today’s globally synchronized surge in inflation, for they are getting a boost in their salaries, but retirees are living their nightmares. Retirees want inflation protection in their retirement years and protection from longevity risk.

Design

In this experiment, we consider a new product design composed of a whole life level annuity and an increasing annuity. The purpose of the increasing annuity is to mimic the effect of inflation.

The simplicity of the increasing annuity design is quite evident. The annual benefit amount of the increasing annuity is k, 2k, 3k, 4k,… for year 1, 2, 3, 4,… and so on. On the other hand, the additional cash necessary to keep up with inflation would be [exp(f*t) – 1] where f is the inflation rate. For the whole life annuity, the annual benefit amount stays constant.

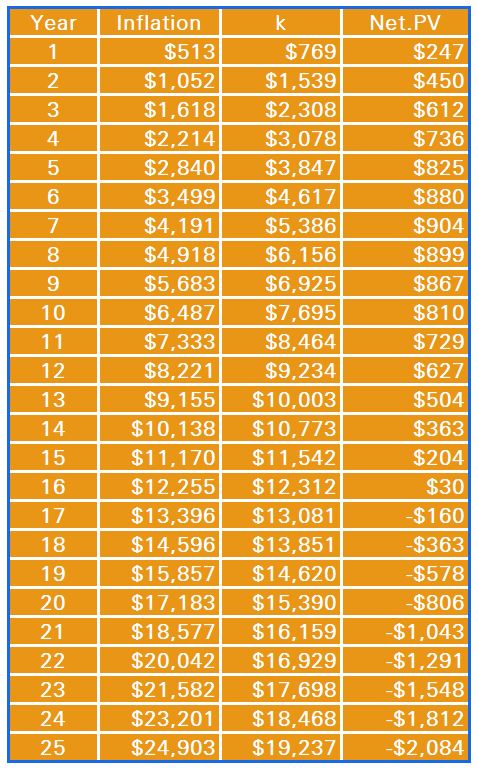

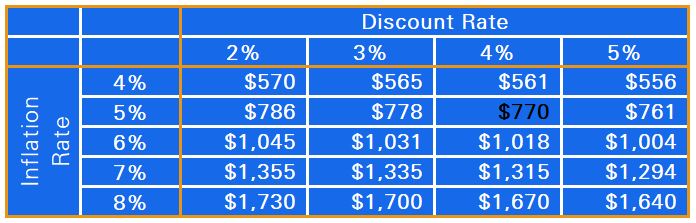

Using an inflation rate and a discount rate, we determine the level of k that will minimize the present value of the difference between the Inflation Coupon amount [exp(f*t) – 1] and the Increasing Annuity Benefit (k, 2k, 3k,…). For example, in the table below, the annual benefit of level annuity is $10,000, inflation rate is 5%, discount rate is 4% and the inflation protection runs for 25 years.

Table 1 : Using the variables above (inflation = 5%, Discount Rate = 4%, level benefit = $10,000), we determine k to be ~$770. The same is shown in Figure 1 below. Continuous compounding is used for this calculation (only).

Inflation (Coupon) is the additional cash (interest) that an annuitant would need to keep up with inflation. Simply, it is $10,000 *[exp(0.05*t) – 1]

k is the initial benefit amount (of increasing annuity) determined by setting sum(Net.PV) =0.

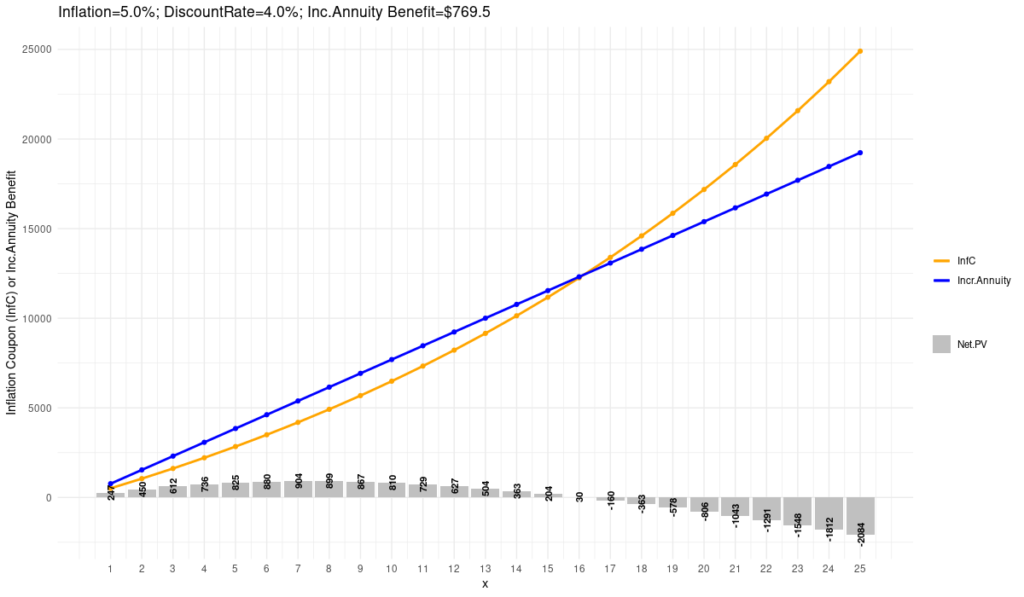

Figure 1 : Blue line shows Increasing Annuity benefit(k,2k,3k,...) overtime. k = $769.5. Orange line shows the inflation Coupon amount given inflation = 5%. Net PV is a small fraction of the annual benefit amount. Sum of Net.PV = 0.

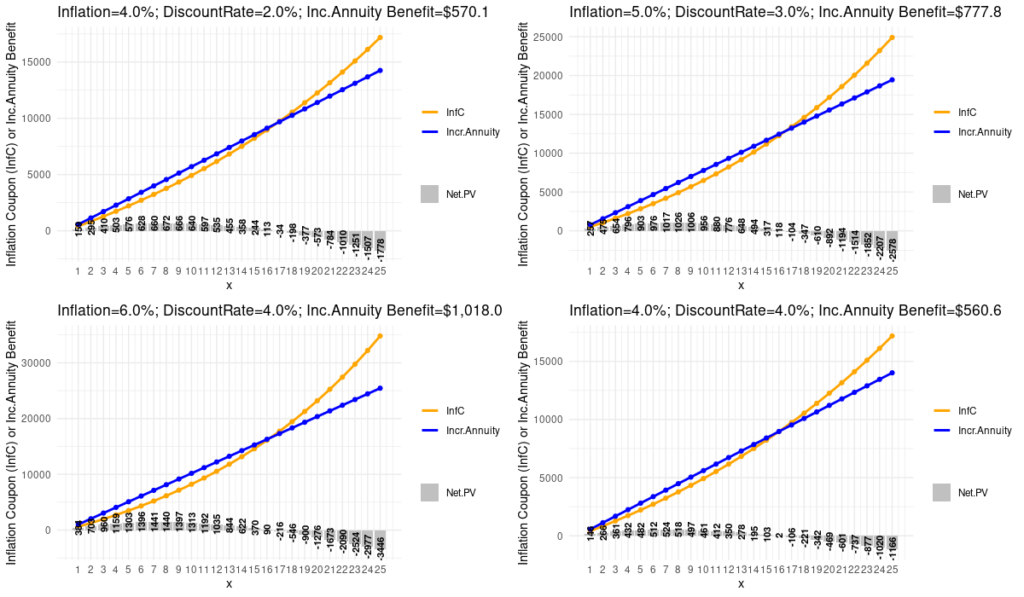

Figure 2: We run the same optimization(search for k) for different combinations of inflation and Discount Rates. Blue line shows increasing Annuity benefit(k, 2k, 3k..). k is shown in each chart title. Orange line shows the inflation Coupon amount given different inflation rates. Inflation rate is >= Discount rate, to reflect accommodative monetary policy stance. Sum of Net.PV = 0 for each chart.

Table 2: For different combinations of inflation and Discount Rates, we determine the level of k that would be necessary to keep up with inflation. k runs over 25 periods. Continuous compounding is use.

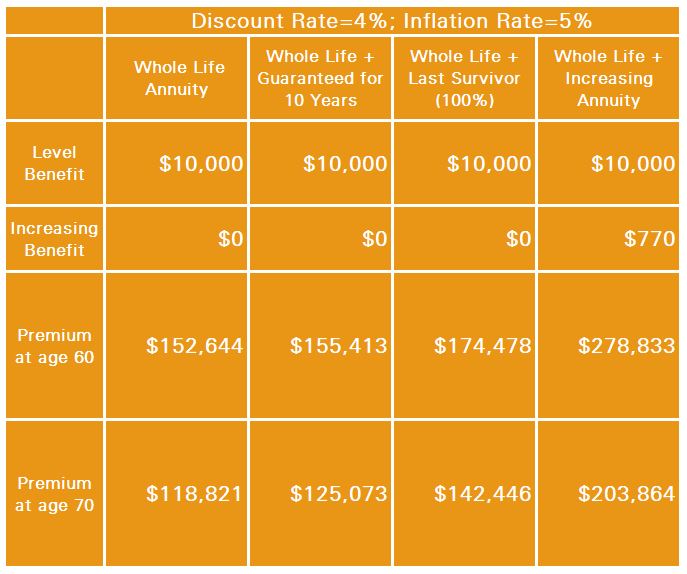

Table 3: Finally, we compare the upfront premium (reserve) for an immediate annuity starting at age 60 to 70, and the annual pension amount set at $10,000.

Analysis

The premium (reserve) amount required for the Inflation Protected (IP) annuity is 1.7x – 1.8x times the premium required for a whole life immediate annuity. Another issue is that the benefit amount increases with time, leading to a higher mortality credit, and making the product less appealing for those who prefer bequest over insuring longevity+inflation risk.

On the other hand, the IP annuity’s starting benefit is higher ($10,770 vs $10,000 for the rest). We believe that the simplicity of this product and the built-in inflation hedge will be appealing to annuitants and agents alike. For insurers, having this payout will add to the product assortment and will likely draw in customers.