Our analysis clearly shows that asset income is the primary determinant of insurers ROE for both FA and FIA. The current regime of high rates and average asset and equity returns present excellent conditions for both policyholder and insurers. While low equity returns reduce policyholders’ payoffs, they do not affect insurers’ income as long as spread income is sufficient. Finally, spread income lower than 75 bps spells doom for FA and FIA insurers alike, while policyholders continue to earn average payoffs.

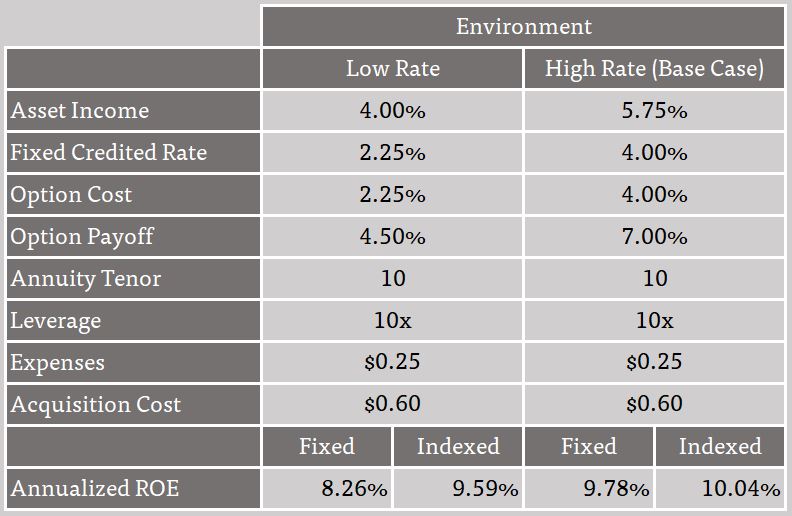

Table 1: Comparison of Base case (Current Regime) with a Low Interest Rate macro environment.

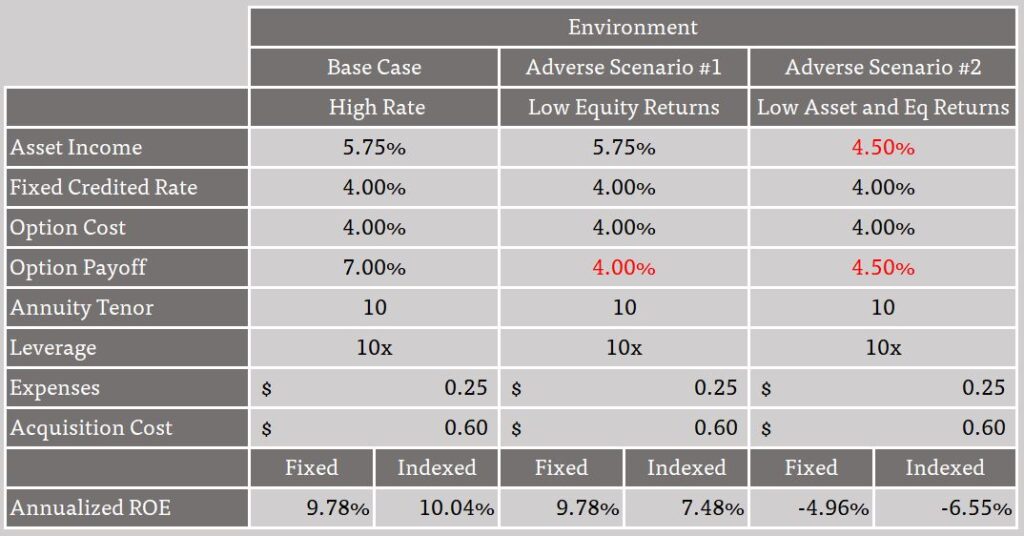

Table 2: Two adverse scenarios are shown. Asset returns (credit income) are the primary determinant of insurer's income

Assumptions and Analysis

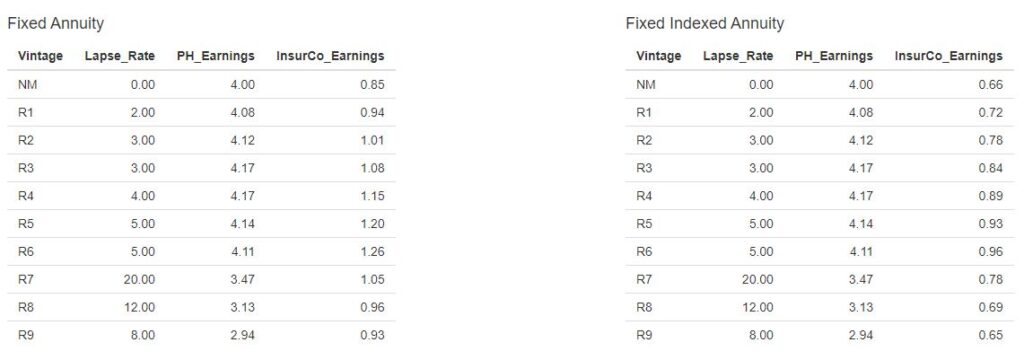

In this analysis, we compare the expected policyholder payoffs and business returns for Fixed Annuity (FA) and Fixed Indexed Annuity (FIA) providers. We ignore the impact of taxes (Bermuda, ahem). The first year’s premiums are called a New Money (NM), and subsequent renewals are called as R1, R2, R3… and so on, somewhat like vintage years (borrowed from PE).

We also model policy lapses in the later years, which reduce the asset balance of the insurer. The lapse rates we have used are 0%, 2%, 3%, 3%, 4%, 5%, 5%, 20%, 12%, 8% for years 1 to 10, respectively. The surrender charge goes away after 7th year, which leads to a much higher lapse rate (20%) in the 8th year.

Option Budget is determined using the current 5-year US corporate A rated yield. We set fixed annuity rates equal to option budget, determined using 5 year US Corporate yield. Option budgets further determine FIA caps. So, a 2.25% option budget sets the cap at 4.5%, while a 4% option budget sets the cap at 7%. These caps are based on European Vanilla (point-to-point) options on S&P 500 Index.

We set book leverage to 10x. A 10x leverage means the ratio of ‘Assets’ to ‘Shareholder Equity’ is 10. Acquisition cost is 60 bps per year, and expenses are 25 bps per year.

Another key assumption that applies to Asset Income, Option Budgets and Option Payoffs is that all these rates are flat and fixed at a constant level (unchanging).

Finally, for further simplicity, we assume that credit income determines asset income; and the performance of S&P 500 determines equity returns.

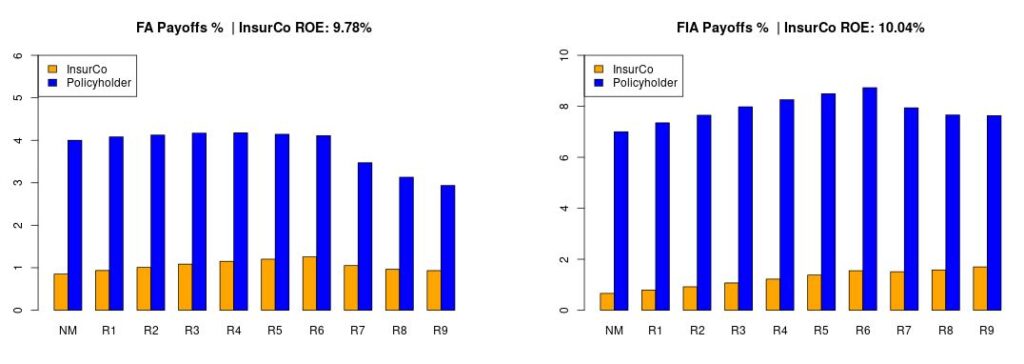

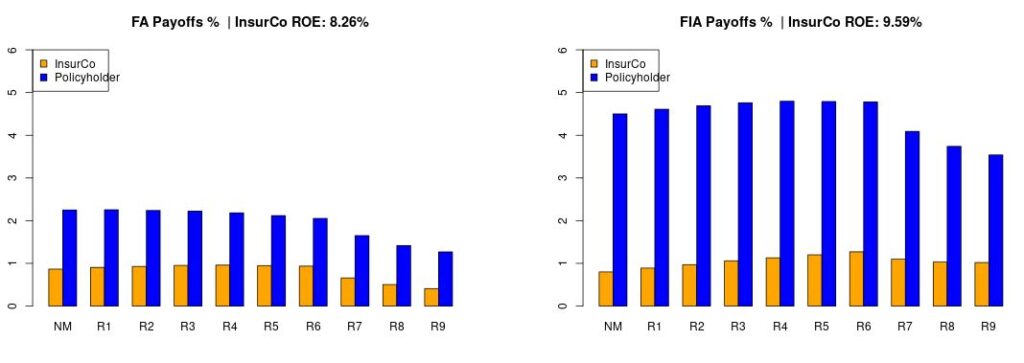

Base Case Scenario: The Current Macro Environment of High Rates and Average Asset and Equity Returns bodes well for annuity providers and policyholders alike.

Now that we are decidedly in a regime of higher interest rates, let’s call it the “Base Case” macro environment. Equity returns of 7%-9% are low relative to the recent history, but sufficient to max out the FIA caps. Likewise, we (conservatively) expect moderate credit income and asset returns at 5.75%. Thus, this macro environment creates ideal conditions for both policyholders’ (maxed out caps) and insurers’ returns from FA and FIA products.

Base Case : High Interest Rates and Moderate Asset Returns

Base Case: High Interest Rates and Moderate Asset Returns

Low Rate Environment : Low Interest Rates and moderate asset and equity returns

Chart: Low rate macro environment

Table : Low rate macro environment

Adverse Case Scenario: Asset Income (not equity returns) is the primary determinant for insurers' income from FA and FIA products.

We study two different scenarios.

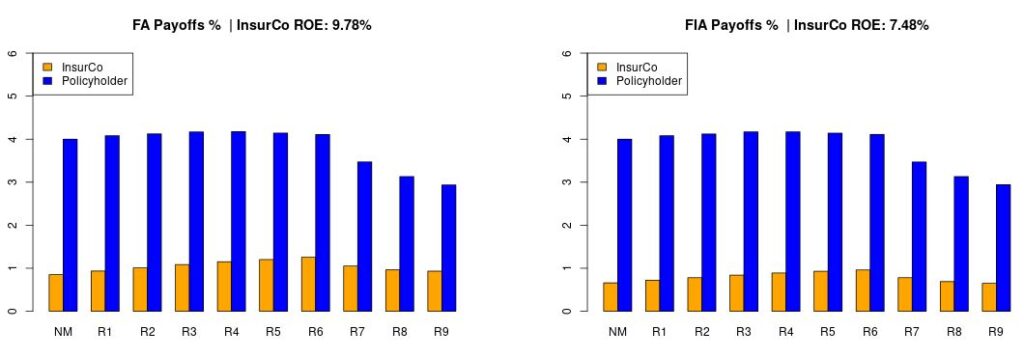

Adverse Scenario #1: Low Equity Returns.

The only difference between the Base Case scenario and the Low Equity Return scenario is that of Option Payoff (reduced from 7% to 4%). Based on last 20 years’ of historical data, annualized equity returns of 5% or less represent cumulative frequency of less than 25%. Meaning there is a 75% chance that equity returns will be higher than 5%. So, a 4% equity return is a reasonable approximation of low EQ return scenario. The main effect is on policyholders’ payoffs. Secondarily, because of lower growth in general account, the insurers’ FIA incomes also suffer.

Chart : Adverse Scenario #1

Table: Adverse Scenario #1

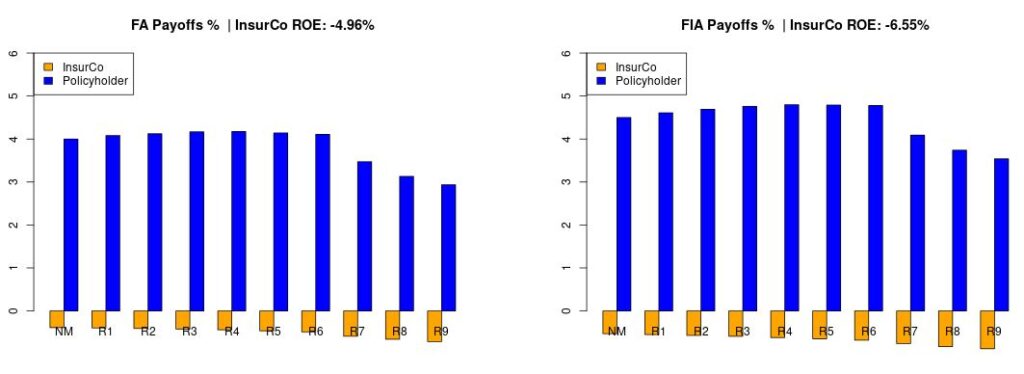

Adverse Scenario #2: Low Asset Returns and Low Equity Returns

Here, we assume lower asset income (5.75% -> 4.5%) and lower equity returns (7.0% -> 4.5%) compared to our Base Case scenario. Our reason for combining low equity returns with low asset returns in this scenario is that, we think going forward, it will be very unlikely to see a combination of low credit income (low asset returns) and high equity returns. A significant Central Bank easing could achieve such a scenario (low asset income, high equity income), but we would like to exclude that possibility. In a realistic Adverse Case scenario, credit losses will invariably spill off to equity markets, lowering equity returns. Since insurers are quite conservative in their asset book, they will still earn an average of 50 bps over 5 year US Corporate A yield despite significant credit losses stretching over 2-4 years. Here, we see that while policyholders earn average payoffs, the insurers’ return are deeply negative. The main reason for this outcome is the low spread earned by insurers (4.5% – 4% = 0.5%), which is not enough to pay for acquisition costs and expenses. This result highlights two key phenomena: 1) FA and FIAs are invariably “spread products” as long as insurers’ incomes are concerned. 2) Policyholders will continue to earn decent interest income from both FA and FIA in most scenarios.

Chart: Adverse Scenario #2

Table: Adverse Scenario #2

Conclusion

It is quite natural to assume that insurers will lower credited rates and option budgets in an environment of low or negative business returns. Yes, that is quite possible – however, disintermediation risk will limit insurer’s ability to move down rates. Also, many FA products have multi-year guarantees. Also, let’s not forget that in a scenario of severe cash drain, insurers can just discount their policies to earn a whole lot of new money (new policies) in a short amount of time, and later perhaps pierce bailout rates or staple free GLWB riders to those discounted policies. Who doesn’t like this business!